Nzs treasury trap.

As a 52 year old kiwi historian, one of the questions of my life has been

“Why is my lived experience of Nz since 1984 at odds with the promises and talk of the political class, media class, and economics class?”

Accordingly I have paid close attention to life in general, and studied politics and economics in detail. But it still didn’t help me to understand the mechanism of our decline; a decline which is now acknowledged and dated by Treasury to the ‘reforms’ of ruthenasia; and usually obscured by the sugar rush economics of migration and a house price bubble.

However treasury to not name the cause of our woes, nor do they name the mechanism.

It’s the absence of public credit for capital development. It’s the laws of ruthenasia that constrict our nation, and bind us to mismeasurement.

RBNZ credit is how every budget gets filled. It’s not taxes that ‘pay’ for our govt budgets. It’s rbnz credit.

The fact of the matter is this.

“Gold is money, everything else is credit”

JP Morgan

What matters is who gets to create credit (money), and what is it used for?

Ruth Richardson is a champion of the 1%, they acknowledge that her ‘reforms’ were ‘constitutional law - amendments’; while we all remain oblivious to the fact that a nation with an ‘unwritten constitution’ like Nz effectively lacks a constitution; and constitutional powers are the sword and shield of a nation.

Or, in ruthrnasias case, the Trojan horse that allows for the capture of our economy by a private sector that seeks only profit, and lacks any public service motive.

Jim Bolger was the PM who enabled ruthenasia - against his better judgement - and in 2017 he labelled it a failure.

Meanwhile, those who Muldoon called ‘the greedies’ are gearing up for a second/third/fourth bite at the nation under the guise of ‘asset recycling’- because Nz ‘has no money’.

But as the LSAP and JP Morgan show us, ‘money’ is not the problem.

The problem is the constitutional law amendments that are destroying our productive capacity and ability to prosper.

It’s taken me three years to prove it in an evidence model that I call the treasury trap.

Please find it here.

It’s summarised in the first two pages

Treasury dates NZs economic reforms of the 1990s as having led to low public investment, low productivity, high public debt, a brain, skills, and population, drain. Although they don’t name it as such, it is, instead, simply a chronological correlation; rather than a directly observed link to ‘the far reaching reforms’ that many kiwis called ‘Ruthenasia’ which occurred at that time; reducing our national sovereignty, public wealth, public infrastructure and productive development.

Institutional mis-measurement hides housing-credit inflation; and, (with public development credit disappeared) private mortgage lending becomes the dominant channel of credit creation, shaping the structure of the economy into low risk speculative extraction. Rents.

While we don’t build what we need.

Self styled ‘entrepreneurs’ of the right wing acknowledge these as deliberate constitutional law amendments that changed our economic architecture. To ‘protect it from democracy’.

The economic reforms called ‘rogernomics’ and ‘ruthenasia’ have led to broad and measurable underinvestment in essentials and productive industries; economic inequality, increased poverty, strategic fragility, political immaturity, de-industrialisation, an annual haemorrhaging of our wealth overseas that equals 20% of our total exports, and a cost of living that consumes four fifths of most people’s income.

Prime Minister at the time, Jim Bolger, had to be almost coerced into many of the reforms by his finance minister and treasury, and he called them a failure before his death.

Legally, they seem to breach the duty of care, fiduciary duty, and duty to use honest rights and measures. To name only three.

The biggest winners are Australian banks.

Historian Tadhg Stopford calls it

The Treasury Trap

The Treasury Trap is a constitutional misalignment between sovereign authority and the architecture of capital formation.

Hidden in plain sight, it explains the economic trajectory of Nz since it’s far reaching reforms of 1984-1994

When mis-measurement by public authorities obscures the dynamics of housing-credit inflation and the rising costs of essential goods and services, and when public development-credit institutions disappear/are removed/privatised without replacement,

private mortgage lending becomes the dominant channel of credit creation.

Aka Australian banks create 97% of the money/credit in our economy.

As interest bearing debt for ever more expensive houses.

Because, in such a system, the allocation of new purchasing power increasingly follows collateral incentives in land markets rather than the long-term capital-formation needs of the nation.

The structure of the economy is therefore shaped by private mortgage finance rather than by institutions responsible for national development.

We live with the consequences; a public infrastructure deficit of more than two hundred billion dollars, and an increasingly unhappy country

Because, in large part, under the Public Finance Act 1989, New Zealand adopted accrual accounting and budgeting.

Public investment increases both assets and liabilities on the Crown balance sheet.

Left pocket, right pocket, but one pockets providing a return over time.

However fiscal frameworks and political discourse emphasise liability indicators such as public debt ratios.

As a result, long-lived public investments that create productive national assets are frequently interpreted primarily as increases in government debt.

This accounting-policy interaction has discouraged sovereign capital formation even though investments expand national productive capacity.

Taken together, these institutional arrangements alter the constitutional balance of economic governance.

The state retains formal authority over currency, banking regulation, fiscal policy, and national accounting frameworks, yet the practical direction of credit creation and capital formation shifts toward private balance-sheet incentives.

Where public institutions once exercised responsibility for directing development credit toward infrastructure, housing supply, and productive industry, the absence of such institutions leaves the allocation of new credit largely to collateral-driven mortgage lending.

These developments raise constitutional questions concerning the exercise of sovereign economic powers. Governments exercising authority over monetary institutions, financial regulation, and fiscal frameworks owe duties of fiduciary stewardship, reasonable care in institutional design, and adherence to the long-standing principle of honest weights and measures in public economic measurement. If measurement systems fail to capture dominant cost pressures affecting households, and if institutional arrangements allow credit creation to be directed primarily toward asset inflation rather than productive capital formation, the alignment between sovereign authority and public purpose becomes weakened.

The constitutional implication is not that markets or private finance are illegitimate. Rather, it is that the institutional architecture governing measurement, credit creation, and capital formation must preserve the state’s capacity to steward long-term national development. When the measurement constitution obscures key economic pressures, the credit constitution delegates most money creation to collateral-driven private lending, and the capital-formation constitution constrains sovereign investment through fiscal interpretation of accounting rules, the result can be a structural misalignment between public authority and economic outcomes.

This thesis therefore examines how the interaction of measurement regimes, credit-creation structures, and fiscal-accounting frameworks has reshaped New Zealand’s economic constitution since the late twentieth-century reforms, and how those institutional arrangements influence the direction of capital formation, the distribution of financial risk, and the long-term productive capacity of the nation.

Core Evidence Ledger and solution pathway follows after Panel 3 (below).

Panel 3 Sources at end of full text

TBLR CORE LEDGER

CAPITAL FORMATION CONSTITUTION MODULE

I. GOVERNING PRINCIPLE

Economic prosperity depends on the accumulation of productive capital.

Productive capital includes:

• infrastructure

• housing stock

• industrial capacity

• agricultural systems

• energy systems

• technological capability

• human capital formation.

The process by which societies build these assets is called capital formation.

Capital formation therefore determines the long-run productive capacity of the economy.

II. DEFINITION — CAPITAL FORMATION

Capital formation is the process by which financial resources are converted into durable productive assets.

These assets generate future economic output.

Examples include:

• transport infrastructure

• energy infrastructure

• housing construction

• manufacturing facilities

• irrigation and agricultural investment

• digital infrastructure.

Capital formation is therefore distinct from consumption expenditure.

III. SOURCES OF CAPITAL FINANCE

In modern economies, capital formation can be financed through several mechanisms.

retained corporate earnings

household savings

government borrowing

public development credit

private bank credit creation

foreign capital inflows.

Each mechanism produces different institutional consequences.

IV. CREDIT AND CAPITAL FORMATION

Modern economies rely heavily on credit creation to finance capital formation.

Credit creation expands purchasing power and allows investment before prior savings exist.

This process enables:

• infrastructure development

• housing construction

• industrial expansion.

Therefore the institutional structure governing credit creation strongly influences capital formation.

V. CREDIT ALLOCATION

Credit creation alone does not determine capital formation.

The allocation of credit determines where investment occurs.

Credit allocation mechanisms may include:

• market-based lending

• policy-directed lending

• development banks

• public investment programmes

• fiscal infrastructure investment.

Where credit flows determines which sectors expand.

VI. HISTORICAL DEVELOPMENT FINANCE

Many countries historically developed institutions to direct credit toward national development.

Examples include:

• German development banking institutions

• Japanese industrial finance institutions

• South Korean development banking systems

• United States Reconstruction Finance Corporation

• agricultural credit systems in multiple countries.

These institutions were designed to support sectors where private lending was insufficient.

VII. NEW ZEALAND DEVELOPMENT CREDIT HISTORY

New Zealand historically possessed institutions that directed credit toward development.

These included:

• State Advances systems

• Housing Corporation mortgage programmes

• Development Finance Corporation

• sectoral credit programmes.

These institutions financed:

• housing supply

• agricultural expansion

• industrial investment

• infrastructure development.

This created a sovereign development-credit ecology.

VIII. INSTITUTIONAL ROLE OF DEVELOPMENT CREDIT

Development credit institutions perform several functions.

They can:

finance long-term projects

support sectors with long investment horizons

provide countercyclical lending

support national infrastructure development.

These functions often involve time horizons longer than typical commercial bank lending.

IX. PRIVATE BANK CREDIT ALLOCATION

Commercial banks allocate credit according to risk and collateral.

Bank lending decisions are influenced by:

• collateral quality

• regulatory capital requirements

• borrower creditworthiness

• short-to-medium-term profitability.

Assets with secure collateral are more likely to receive credit’s.

X. LAND AS COLLATERAL

Land possesses characteristics that make it attractive collateral for banks.

These include:

• immobility

• legally enforceable title

• durability

• historically rising value.

Because of these characteristics, lending secured against land is perceived as relatively low risk.

This creates a structural incentive for banks to concentrate lending in property markets.

XI. CREDIT–ASSET FEEDBACK

Mortgage lending expands purchasing power in housing markets.

Higher purchasing power increases housing demand.

Increased demand raises land prices.

Rising land prices increase collateral values.

Higher collateral values support further mortgage lending.

This creates a credit–asset price feedback loop.

XII. CAPITAL MISALLOCATION RISK

When credit allocation is dominated by property lending, several structural risks arise.

These include:

• underinvestment in productive industry

• infrastructure funding gaps

• housing affordability deterioration

• rising household leverage.

These risks emerge because credit is directed toward existing assets rather than new productive capacity.

XIII. PUBLIC INVESTMENT AND INFRASTRUCTURE

Infrastructure projects often require:

• large upfront investment

• long asset lifetimes

• stable financing.

Because infrastructure benefits are widely distributed across society, private financing alone may be insufficient.

Public investment has historically played a major role in infrastructure development.

XIV. FISCAL RULES AND INVESTMENT

Public investment capacity is influenced by fiscal rules.

These rules may include:

• debt limits

• deficit targets

• accounting frameworks.

When fiscal frameworks emphasise liability indicators alone, public capital investment may be politically constrained.

XV. ACCOUNTING AND CAPITAL FORMATION

Accrual accounting records the full balance-sheet effects of public investment.

Public investment increases both:

• public assets

• public liabilities.

However public debate often focuses primarily on liability measures such as public debt.

This emphasis can discourage long-term capital investment.

XVI. FOREIGN CAPITAL

Foreign capital can also finance domestic investment.

Foreign financing may take the form of:

• direct investment

• portfolio investment

• bank lending

• sovereign borrowing.

Foreign capital can support development but may also create:

• profit repatriation

• interest outflows

• external financial vulnerability.

XVII. EXTERNAL BALANCE AND CAPITAL FLOWS

When domestic investment exceeds domestic savings, economies rely on foreign capital inflows.

Persistent reliance on external capital can produce a net primary income deficit, reflecting ongoing income outflows to foreign investors.

XVIII. CAPITAL FORMATION AND ECONOMIC STRUCTURE

The sectors receiving investment shape the structure of the economy.

Investment concentrated in:

• housing assets

• land price appreciation

produces a different economic structure than investment concentrated in:

• infrastructure

• productive industry

• technological development.

Thus credit allocation influences long-term national development.

XIX. NEW ZEALAND STRUCTURAL QUESTION

If

• public development-credit institutions decline

• fiscal rules discourage sovereign investment

• commercial banks allocate most credit toward property collateral

then the institutional mechanism directing capital toward national development becomes unclear.

This raises a structural governance question.

XX. THE CAPITAL FORMATION QUESTION

The central question of the capital formation constitution is:

Which institutions direct investment toward the long-term productive capacity of the nation?

Possible answers include:

• public investment institutions

• development finance institutions

• coordinated industrial policy

• market allocation through private finance.

The choice of institutional arrangement determines national development outcomes.

XXI. CAPITAL FORMATION AND THE ECONOMIC CONSTITUTION

Measurement systems determine how the economy is perceived.

Credit architecture determines how investment is financed.

Capital formation rules determine what is built.

Together these elements constitute the economic constitution.

XXII. LEDGER RULE

Future analysis of economic policy must distinguish between:

• consumption spending

• capital formation

• credit creation

• credit allocation

• asset price inflation.

Failure to distinguish these categories produces analytical smudging.

XXIII. CONSTITUTIONAL CONCLUSION

If a nation lacks institutional mechanisms capable of directing credit toward productive investment, then capital formation will depend largely on the incentives of private finance.

Where those incentives favour collateralised assets such as land, investment may concentrate in property markets rather than productive development.

The institutional architecture governing credit and investment therefore determines the long-run structure of the economy.

TBLR CORE LEDGER v3.1

Constitutional Architecture of Credit, Measurement, and Capital Formation

FIRST PRINCIPLE

Credit Creation Determines Investment

In modern monetary economies, money enters circulation primarily through credit creation.

The authority to create credit determines where new purchasing power appears.

Where new purchasing power appears determines where investment occurs.

Investment allocation determines:

• the structure of the economy

• the distribution of wealth

• the rate of capital formation

• long-term economic productivity.

Therefore:

Who creates money determines where investment occurs.

Where investment occurs determines the structure of the economy.

For this reason:

Credit architecture functions as a hidden constitution of the economic system.

MODULE I

Sovereign Economic Powers

Modern states exercise authority over several core economic institutions.

These include:

monetary institutions governing currency issuance

regulation of banking and credit creation

authority over taxation and sovereign borrowing

determination of national accounting frameworks

authority over financial regulation.

These authorities constitute delegated sovereign powers.

Because these powers shape the structure of the economy, they fall within the constitutional domain of public governance.

MODULE II

Constitutional Duties in Economic Governance

When governments exercise sovereign economic powers, several duties arise.

Fiduciary Duty

Public authorities must exercise economic powers in the long-term interest of the nation.

This includes stewardship of national economic stability, prosperity, and development capacity.

Duty of Care

Economic institutions must be designed with reasonable competence and awareness of foreseeable systemic consequences.

Institutional negligence in economic design can produce structural instability.

Honest Weights and Measures

Governance requires accurate measurement of the phenomena being regulated.

The principle of honest measurement is ancient and universal.

Examples include:

• ancient Near Eastern commercial codes regulating trade measurement

• biblical injunctions against false weights and measures

• Greek and Roman laws governing market standards

• medieval European statutes on measurement fairness

• early modern state regulation of coinage and standards.

Across millennia, societies recognised that economic governance requires reliable measurement.

If measurement systems misrepresent economic reality, policy becomes structurally distorted.

MODULE III

Core Domains of Economic Architecture

Four institutional domains determine the structure of modern economies.

credit creation systems

credit allocation mechanisms

monetary policy frameworks

economic measurement systems.

These domains jointly determine:

• investment patterns

• capital formation

• financial stability

• distribution of prosperity.

MODULE IV

Pre-Reform Credit Architecture

Before the late twentieth-century reforms, New Zealand’s financial system contained multiple channels of credit creation.

These included:

government borrowing

sovereign development credit

private bank credit.

These mechanisms together produced a diversified credit architecture.

MODULE V

Sovereign Development-Credit Ecology

Public institutions historically directed credit toward national development.

These institutions included:

• State Advances lending systems

• Housing Corporation mortgage lending

• Development Finance Corporation

• agricultural credit programmes.

These institutions financed:

• housing construction

• infrastructure development

• agricultural investment

• industrial expansion.

This network constituted a development-credit ecology.

Through this ecology, the state possessed institutional capacity to influence the direction of capital formation.

MODULE VI

Financial Liberalisation

During the reform period financial markets were liberalised.

Key policy changes included:

• removal of interest-rate controls

• removal of credit ceilings

• removal of exchange controls.

These reforms allowed commercial banks to expand lending balance sheets more freely.

Private bank credit creation therefore became the dominant credit channel.

MODULE VII

Withdrawal of Sovereign Development Credit

During the reform period, public development-credit institutions were dismantled or commercialised.

Examples include:

• liquidation of the Development Finance Corporation

• removal of state mortgage lending channels

• decline of government-directed credit programmes.

Result:

government-directed domestic investment credit declined sharply.

The sovereign development-credit ecology ceased to function.

MODULE VIII

Fiscal Accounting Transformation

Public financial management shifted toward accrual accounting.

Public capital investment increases both public assets and public liabilities.

However fiscal policy discourse focuses heavily on liability indicators such as public debt ratios.

As a result, public capital formation increasingly appeared politically as fiscal liability.

This altered political incentives surrounding sovereign investment.

Under the Public Finance Act 1989, New Zealand adopted accrual accounting and budgeting. Public investment increases both assets and liabilities on the Crown balance sheet. However fiscal frameworks and political discourse emphasise liability indicators such as public debt ratios.

This has discouraged sovereign capital formation even when investments create productive assets.

New Zealand moved from a system where the state actively created and directed development credit to one where private banks create most new money and sovereign investment is politically constrained by fiscal rules interpreted through accrual accounting metrics.

MODULE IX

Monetary Policy Framework

Institution:

Reserve Bank of New Zealand.

Primary policy instrument:

Official Cash Rate.

The OCR influences the price of credit through interest rates.

It affects:

• mortgage borrowing costs

• business lending rates

• financial market interest rates.

However:

The OCR does not determine the allocation of credit across sectors.

Credit allocation therefore follows the incentives of lending institutions.

MODULE X

Measurement Architecture

Inflation targeting relies primarily on the Consumer Price Index.

Institution:

Statistics New Zealand.

CPI measures consumer consumption prices rather than asset prices or financing costs.

CPI excludes several major housing-credit components:

• land prices

• house purchase prices

• mortgage principal repayments

• mortgage interest payments.

Housing costs enter CPI primarily through:

• rents

• maintenance

• insurance

• local government rates.

MODULE XI

Tradables vs Non-Tradables

CPI aggregates two categories of prices.

Tradable goods:

• internationally traded manufactured goods

• electronics

• clothing

• vehicles.

Non-tradable goods and services:

• housing

• utilities

• insurance

• domestic services.

During the globalisation period, prices of tradable manufactured goods declined.

Cheap imported goods therefore exert downward pressure on CPI.

MODULE XII

CPI Masking Mechanism

Because CPI averages tradable and non-tradable goods:

falling prices for imported goods can offset rising domestic costs.

Consequently CPI may remain stable even while:

• housing prices rise

• insurance costs increase

• utilities become more expensive

• mortgage debt expands

• household financial pressure rises.

This masking effect weakens policy feedback.

MODULE XIII

Bank Credit Creation

Commercial banks create deposits when issuing loans.

Loan issuance simultaneously creates:

• a bank asset (loan)

• a bank liability (deposit).

This process expands the money supply.

Bank lending therefore represents the dominant mechanism of money creation in modern economies.

MODULE XIV

Collateral Incentives

Banks allocate credit according to risk and collateral.

Land has several characteristics that make it preferred collateral:

• immobility

• legally enforceable ownership

• durability

• historically appreciating value.

Because of these characteristics, land-secured lending carries relatively low perceived risk.

Therefore bank credit allocation tends to concentrate in property lending.

MODULE XV

Asset Price Feedback

Mortgage credit increases purchasing power in housing markets.

Rising housing prices generate expectations of future appreciation.

These expectations stimulate further mortgage borrowing.

Mortgage borrowing increases housing demand.

The result is a self-reinforcing credit–asset price feedback loop.

MODULE XVI

External Bank Funding

If domestic credit expansion exceeds domestic savings, banks must obtain funding from external sources.

Funding sources include:

• offshore wholesale borrowing

• international capital markets.

Evidence appears in:

• Bank for International Settlements banking statistics

• Reserve Bank financial stability reports.

Mortgage credit expansion therefore increases banks’ reliance on external funding.

MODULE XVII

External Liabilities

Offshore funding increases the external liabilities of the banking system.

Domestic housing leverage therefore becomes linked to international capital flows.

MODULE XVIII

Net Primary Income Deficit

External liabilities produce ongoing income outflows.

These include:

• interest payments

• dividends

• profit repatriation.

New Zealand therefore records a persistent net primary income deficit.

MODULE XIX

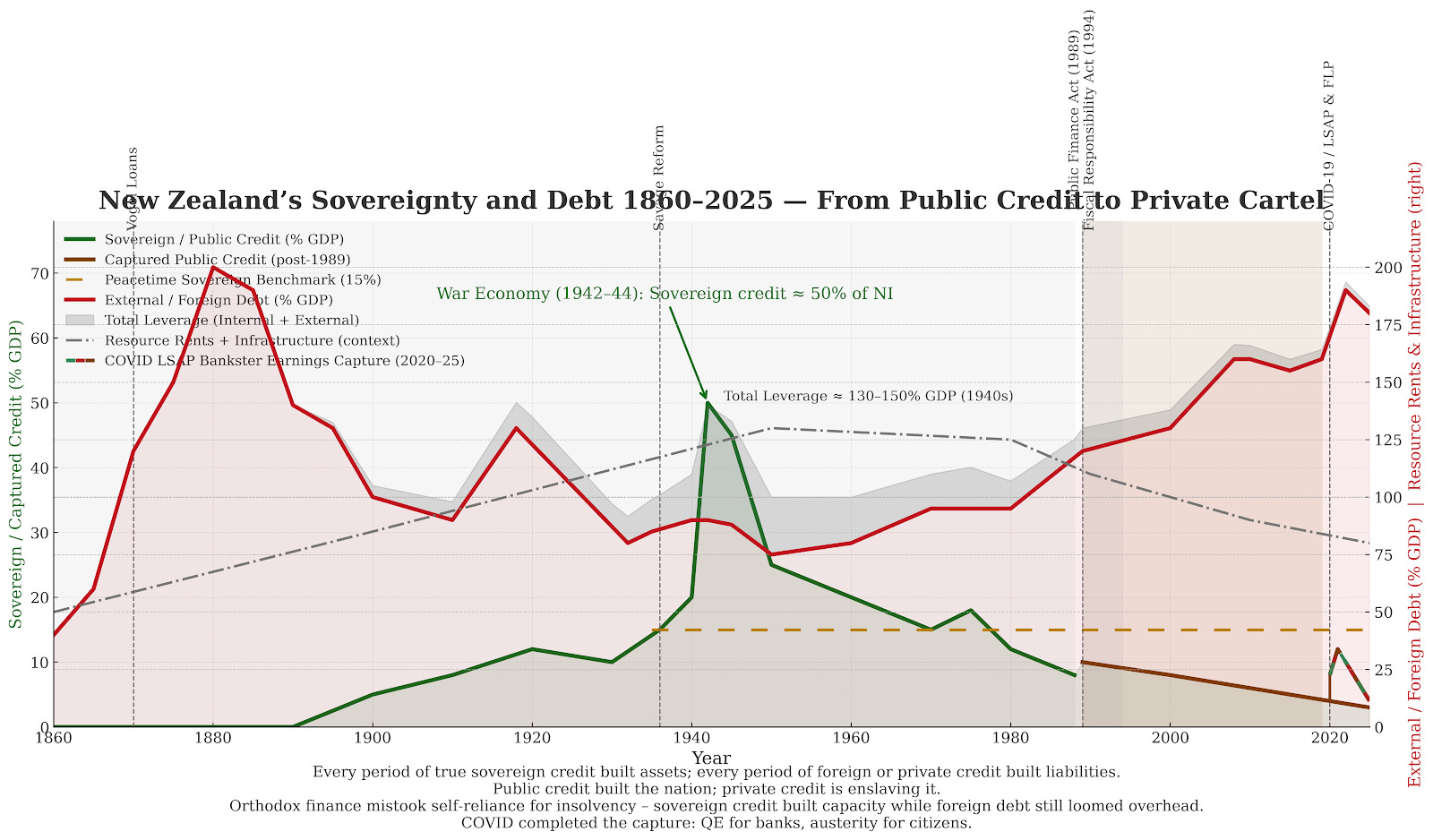

Panel Three — Credit Architecture

Panel Three illustrates the structural evolution of the financial system.

The chart maps three balance-sheet trajectories.

Green line:

Sovereign and public credit.

Brown line:

Residual public credit under the fiscal regime.

Red line:

External liabilities.

Grey shaded area:

Private leverage generated by bank credit creation.

The chart shows a structural shift:

• public development credit declined

• private mortgage credit expanded

• external liabilities increased.

The balance of financial power moved from sovereign institutions toward private mortgage banking.

MODULE XX

Treasury Trap System Loop

Measurement excludes housing credit dynamics

↓

Monetary policy targets CPI

↓

Interest rates adjust price of credit

↓

Private banks dominate credit creation

↓

Collateral incentives favour land

↓

Mortgage lending expands

↓

Housing prices rise

↓

Credit–asset feedback strengthens

↓

Bank funding requirements increase

↓

Offshore funding expands

↓

External liabilities increase

↓

Income outflows increase

↓

Cheap tradable imports suppress CPI

↓

CPI remains stable

↓

Policy perceives inflation under control

↓

System persists.

MODULE XXI

Structural Economic Consequences

The system produces several long-run outcomes.

These include:

rising household leverage

concentration of wealth in housing assets

capital misallocation toward land

diminished sovereign capacity for capital formation

infrastructure underinvestment

increased exposure to external financial flows

potential productivity stagnation.

MODULE XXII

Historical Precedent — Currency Act 1764

The Currency Act of 1764 restricted colonial paper money issuance in British North America.

Colonial economies had previously issued local paper currencies used to finance domestic economic activity.

The Act curtailed these domestic credit mechanisms.

Economic historians link the restriction to:

• credit shortages

• increased private indebtedness

• economic contraction in several colonies.

These financial tensions contributed to political conflict leading toward the American Revolution.

The episode illustrates a broader structural principle:

when domestic economies lose the ability to generate development credit, private debt expansion often replaces public investment.

FINAL SYSTEM LAW

Measurement

↓

Policy Rules

↓

Incentives

↓

Credit Allocation

↓

Economic Structure

↓

National Outcomes.

MODULE XXI

Panel Three Credit Architecture

Panel Three maps the balance-sheet manifestation of the system.

Green line represents sovereign and public credit.

Brown line represents private bank credit.

Red line represents external liabilities.

The rising brown line reflects the displacement of sovereign development credit by mortgage-dominated private credit creation.

Panel Three therefore represents the displacement of the capital constitution of the economy.

MODULE XXII

Constitutional Diagnosis

If institutional design simultaneously:

removes mechanisms for directing sovereign development credit

transfers credit creation authority to private banks

governs monetary policy through a measurement system that excludes housing credit dynamics

discourages public capital formation through accounting rules

allows mortgage-dominated credit allocation

links domestic leverage to external liabilities

then the state’s capacity to steward capital formation and economic development becomes structurally impaired.

MODULE XXIII

Constitutional Question

The central constitutional question is therefore:

whether an institutional architecture that removes sovereign mechanisms for directing capital formation while obscuring the resulting dynamics through measurement systems remains consistent with the fiduciary obligations of democratic governance.

Below is the corrected canonical system map, regenerated to incorporate all hinges, elephants, and pearls identified in this thread and in the critique.

The structure now follows strict mechanical causal order:

sovereign powers → institutional rules → incentives → credit creation → credit allocation → capital formation → economic structure → outcomes

It also explicitly integrates:

Public Finance Act accounting mechanism

financial liberalisation details

collateral advantage of land

credit-asset capitalisation

external funding feedback

income leakage

Panel Three as capital constitution displacement

credit creation vs funding distinction.

This is written to ledger-grade formal constitutional logic.

MODULE XXIV

ASSET TRANSFER VS CAPITAL FORMATION

Capital formation occurs when financial resources create new productive assets.

Examples include:

• infrastructure construction

• new housing supply

• industrial facilities

• energy systems

• technology development.

By contrast, many financial transactions involve the transfer of ownership of existing assets rather than the creation of new productive capacity.

Examples include:

• purchase of existing housing

• purchase of land titles

• financial asset trading.

Mortgage lending frequently finances the purchase of existing housing stock and land titles.

When credit finances asset transfers rather than new construction, financial leverage increases without corresponding increases in productive capacity.

This distinction is critical for understanding the structural effects of mortgage-dominant credit systems.

MODULE XXV

LAND PRICE CAPITALISATION

Land prices reflect the capitalisation of expected future economic benefits associated with land ownership.

These benefits may include:

• rental income

• development rights

• infrastructure access

• expected price appreciation.

When credit availability expands, purchasing power in land markets increases.

Greater purchasing power raises land prices.

Higher land prices increase collateral values.

Higher collateral values support further borrowing.

This process produces a reinforcing feedback mechanism:

credit expansion

→ rising land prices

→ higher collateral values

→ increased borrowing capacity

→ further credit expansion.

MODULE XXVI

CURRENT ACCOUNT AND CREDIT EXPANSION

When domestic credit expansion exceeds domestic savings, banks must obtain additional funding.

Funding sources may include:

• offshore wholesale borrowing

• international capital markets.

External borrowing increases the external liabilities of the banking system.

These liabilities generate future income outflows through:

• interest payments

• dividends

• profit repatriation.

In macroeconomic accounting:

current account deficit

capital inflow from foreign investors.

Mortgage-dominant credit expansion can therefore contribute indirectly to persistent external deficits.

MODULE XXVII

CONSTITUTIONAL BREACH TEST

Governments exercising sovereign economic powers must satisfy three duties.

Fiduciary Duty

The exercise of public authority must advance the long-term prosperity and stability of the nation.

Duty of Care

Institutional design must consider foreseeable systemic consequences.

Honest Weights and Measures

Measurement systems guiding policy must accurately represent the economic phenomena they regulate.

A constitutional failure may occur when all of the following conditions are present:

measurement systems systematically omit dominant economic pressures affecting households or capital formation

policy institutions rely heavily on those measurement systems

institutional arrangements predictably redirect credit creation toward asset inflation rather than productive investment

governments continue to represent the resulting outcomes as successful policy performance.

Under such conditions the alignment between sovereign authority and public purpose may be materially weakened.

MODULE XXVIII

THE BROWN LINE — CORRECTED INTERPRETATION

Panel Three illustrates the balance-sheet transformation of New Zealand’s financial system.

Green Line

Sovereign and public credit used to finance national development.

Brown Line

Residual public credit under post-reform fiscal constraints.

Grey Area

Private leverage generated primarily through mortgage credit.

Red Line

External financial liabilities.

The rising brown/grey structure reflects the replacement of sovereign development credit with mortgage-dominant private credit creation.

This represents a structural transfer of capital formation power:

from public development institutions

to private mortgage banking.

MODULE XXIX

INSTITUTIONAL RESTORATION QUESTION

If

• sovereign development-credit institutions no longer exist

• fiscal accounting discourages sovereign capital investment

• commercial banks allocate most new credit toward property collateral

• inflation measurement obscures housing-credit dynamics

then the institutional mechanism responsible for directing capital toward national development becomes unclear.

This raises a fundamental governance question:

Which institutions are responsible for directing capital formation toward the long-term productive capacity of the nation?

MODULE XXX

SYSTEM REFORM PRINCIPLE

Institutional reform does not require the elimination of private finance.

Rather, reform concerns the balance of credit architectures.

A resilient economic constitution typically includes multiple channels of capital finance, including:

• private banking

• sovereign public investment

• development finance institutions

• capital markets

• foreign investment.

When one channel dominates capital allocation, structural distortions may emerge.

The challenge of economic governance is therefore to design institutions that maintain a balanced capital-formation system.

TBLR CORE LEDGER

REFORM CONSTITUTION MODULE v3.0

Restoration of Sovereign Capital Formation and Measurement Integrity

MODULE XLII

Purpose of Reform

The Treasury Trap describes an institutional condition in which the architecture of measurement, credit creation, and fiscal governance directs financial resources toward asset inflation rather than productive capital formation.

Under this condition:

• sovereign development credit disappears

• private mortgage credit becomes dominant

• housing leverage expands

• infrastructure investment weakens

• external financial exposure increases.

The purpose of reform is to restore sovereign institutional capacity to guide capital formation toward long-term national development.

Reform does not eliminate private finance.

Reform restores a balanced financial constitution in which multiple credit systems operate simultaneously.

MODULE XLIII

First Principle of Economic Governance

Credit creation determines investment.

Investment determines the structure of the economy.

Economic governance therefore requires institutions capable of influencing the allocation of credit.

Where credit creation becomes concentrated in a single institutional channel, the structure of the economy will follow the incentives of that channel.

MODULE XLIV

Sovereign Economic Dashboard

Economic governance shall be guided by a Sovereign Economic Dashboard.

The dashboard shall measure national performance across five domains.

Measurement Integrity

Indicators include:

• CPI inflation

• household living cost indices

• food price dynamics

• housing price dynamics

• tradables inflation

• non-tradables inflation.

Credit Allocation

Indicators include:

• mortgage credit growth

• business credit growth

• sectoral credit distribution.

Capital Formation

Indicators include:

• infrastructure investment

• housing construction

• industrial investment.

External Balance

Indicators include:

• current account balance

• net international investment position

• foreign funding exposure.

Institutional Integrity

Indicators include:

• transparency compliance

• conflict-of-interest reporting

• institutional independence.

Dashboard data shall be:

• published annually

• audited by the Auditor-General

• publicly accessible.

Persistent deterioration shall trigger mandatory parliamentary review.

MODULE XLV

Honest Weights and Measures

Economic governance depends on accurate measurement.

Legal traditions requiring honest weights and measures appear in:

• ancient Near Eastern law

• biblical law

• medieval market regulation.

Modern economic governance inherits this principle.

Measurement systems must represent the dominant economic forces affecting households and capital formation.

Where measurement excludes key economic pressures, policy decisions become structurally distorted.

MODULE XLVI

Measurement Integrity Institutions

A measurement integrity authority shall review national economic indicators used in policy.

Responsibilities include:

• auditing inflation metrics

• reviewing cost-of-living indicators

• identifying measurement distortions.

The authority shall report annually to Parliament.

MODULE XLVII

Restoration of Sovereign Development Credit

The financial system shall include institutions capable of directing credit toward national development.

Development finance institutions shall provide long-term credit for:

• infrastructure

• energy systems

• housing construction

• industrial development.

These institutions restore sovereign influence over capital formation.

MODULE XLVIII

Hybrid Credit Architecture

A resilient financial system contains multiple channels of credit creation.

These include:

Private bank credit

Sovereign development credit

Public investment

International capital.

Private banks remain central to the financial system.

However private mortgage lending shall not remain the dominant mechanism of capital formation.

Institutional reforms shall therefore ensure the continued existence of sovereign development credit channels.

MODULE XLIX

Housing Capital Formation Reform

Mortgage credit frequently finances transfers of existing housing.

Housing finance reform shall direct credit toward:

• new housing construction

• supporting infrastructure.

This reduces the tendency of mortgage credit expansion to inflate land prices without increasing supply.

MODULE L

Fiscal Capital Accounting

Public investment produces long-lived assets.

Fiscal reporting shall distinguish between:

• consumption expenditure

• capital formation.

Capital investment reporting shall include:

• asset creation

• infrastructure value

• long-term economic return.

This distinction prevents productive investment from being misrepresented as fiscal deterioration.

MODULE LI

External Balance Defence

Domestic credit expansion financed through foreign borrowing increases national external liabilities.

External balance monitoring shall therefore track:

• foreign bank funding exposure

• external debt levels

• international investment position.

Persistent deterioration shall trigger policy review.

MODULE LII

Panel Three

Panel Three illustrates the balance-sheet evolution of the New Zealand economy.

Green line

Sovereign development credit.

Brown line

Constrained sovereign credit following reform.

Grey structure

Private mortgage leverage.

Red line

External liabilities.

Panel Three demonstrates the structural transfer of capital formation authority from public institutions to mortgage-dominant private banking.

MODULE LIII

Historical Precedent

Historical examples demonstrate the consequences of restricting domestic credit creation.

The Currency Act 1764 restricted the American colonies from issuing paper currency.

Economic historians link this restriction to:

• credit shortages

• rising private debt

• economic stagnation.

These pressures contributed to tensions preceding the American Revolution.

The historical lesson is that restricting domestic development credit can shift financial leverage toward private debt.

MODULE LIV

National Dividend

A National Dividend distributes a share of national productivity to citizens.

Funding sources may include:

• sovereign investment returns

• public asset income

• resource rents.

The dividend strengthens the link between citizens and the productive capacity of the national economy.

Final Reform Principle

A resilient economic constitution requires:

• accurate measurement

• diversified credit systems

• sovereign capital formation institutions.

When these conditions are present, financial systems can support both private enterprise and national development.

TBLR SYSTEM MAP (CANONICAL)

Constitutional Architecture of Credit, Measurement, and Capital Formation

LAYER 1 — SOVEREIGN ECONOMIC POWERS

Modern states exercise public authority over several core economic instruments.

These include:

control of currency and monetary systems

regulation of banking and credit creation

authority over taxation and sovereign borrowing

determination of national accounting frameworks.

These powers form the economic constitution of the state.

They determine the institutional rules governing credit, investment, and capital formation.

LAYER 2 — INSTITUTIONAL RULES

Institutional rules determine the operating framework of the financial system.

Four domains are critical.

financial regulation

fiscal accounting rules

monetary policy mandates

economic measurement systems.

These rules shape the incentives faced by financial actors.

LAYER 3 — REFORM ARCHITECTURE

During the late twentieth century reforms, these institutional rules changed simultaneously.

Financial Liberalisation

Key changes included:

• removal of interest-rate controls

• removal of credit ceilings

• removal of exchange controls.

These reforms allowed commercial banks to expand balance sheets and create credit more freely.

Withdrawal of Sovereign Development Credit

Public development-credit institutions were dismantled or allowed to disappear.

Examples included:

• State Advances lending systems

• Housing Corporation mortgage lending

• Development Finance Corporation.

These institutions previously directed credit toward housing construction, infrastructure, and industrial development.

Their removal reduced the state’s institutional capacity to direct capital formation.

Fiscal Accounting Transformation

The Public Finance Act introduced accrual accounting.

Under accrual accounting:

capital investment increases recorded Crown liabilities.

Consequently:

public capital formation appears as government debt.

When fiscal policy targets debt ratios, this accounting treatment creates a political disincentive for sovereign investment.

Monetary Policy Narrowing

The mandate of the

Reserve Bank of New Zealand

shifted toward CPI inflation targeting.

The primary instrument became the Official Cash Rate.

Interest-rate policy governs the price of credit.

It does not determine credit allocation.

Measurement Architecture

Inflation targeting relies primarily on the Consumer Price Index.

Institution:

Statistics New Zealand

CPI measures consumption prices rather than asset prices or financing costs.

CPI excludes:

• land prices

• house purchase prices

• mortgage principal repayments

• mortgage interest payments.

Housing appears mainly through rents and maintenance expenditures.

LAYER 4 — INCENTIVES

Institutional rules create the incentives governing financial behaviour.

Two mechanisms dominate.

Collateral Incentives

Banks allocate credit based on collateral security and risk.

Land possesses several characteristics favouring its use as collateral.

• immobility

• legally secure title

• durability

• historically appreciating value.

These properties reduce perceived lending risk.

Therefore bank credit allocation gravitates toward land-secured lending.

Measurement Incentives

Because CPI excludes housing credit dynamics and averages domestic prices against imported goods, policy feedback from inflation targeting does not fully capture housing-credit inflation.

This reduces policy response to mortgage-driven asset inflation.

LAYER 5 — CREDIT CREATION

Commercial banks create deposits when issuing loans.

In modern banking systems this mechanism constitutes the dominant form of money creation.

After the withdrawal of sovereign development-credit institutions, banks became the primary creators of new domestic credit.

LAYER 6 — CREDIT ALLOCATION

Bank lending decisions follow collateral incentives.

Reserve Bank lending statistics indicate approximately:

60–65 percent residential mortgage lending

25–30 percent business lending.

However significant portions of business lending are also secured against property, including:

• agricultural land mortgages

• commercial property loans

• development finance.

Consequently the banking system has substantial exposure to property collateral.

LAYER 7 — CREDIT–ASSET CAPITALISATION

Mortgage credit increases purchasing power within land markets.

Land prices rise when credit supply increases.

Higher land prices capitalise expected rents and future appreciation into asset values.

This produces a feedback mechanism:

credit expansion → higher land prices → increased borrowing capacity → further credit expansion.

LAYER 8 — CREDIT CREATION VS FUNDING

Credit creation and bank funding are distinct processes.

Banks create credit when lending.

Balance sheet funding may originate from:

• domestic deposits

• offshore wholesale borrowing.

Mortgage credit expansion increases bank funding requirements.

LAYER 9 — EXTERNAL FUNDING FEEDBACK

New Zealand banks rely significantly on offshore wholesale funding.

Evidence appears in:

• BIS cross-border banking statistics

• Reserve Bank financial stability reports.

Mortgage credit growth increases offshore borrowing.

Offshore funding availability also enables further domestic credit expansion.

This creates a bidirectional relationship between credit growth and external funding.

LAYER 10 — EXTERNAL LIABILITIES AND INCOME FLOWS

Offshore funding increases external liabilities.

External liabilities generate income outflows through:

• interest payments

• profit repatriation

• foreign investment income.

New Zealand records persistent net primary income deficits, commonly approximating five to seven percent of GDP.

LAYER 11 — POLICY FEEDBACK FAILURE

Because CPI excludes housing-credit dynamics, rising housing prices and mortgage leverage may occur without corresponding CPI inflation.

Monetary policy therefore receives incomplete information about credit-driven inflation.

Interest-rate adjustments affect borrowing costs but do not change structural credit allocation.

LAYER 12 — CAPITAL FORMATION EFFECT

Credit allocation determines capital formation.

Mortgage lending primarily finances the transfer of ownership of existing land assets rather than the creation of new productive capital.

Consequently:

credit flows toward land ownership rather than infrastructure, industrial investment, or export capacity.

LAYER 13 — STRUCTURAL ECONOMIC OUTCOMES

The system produces several long-term structural outcomes.

rising household leverage

housing-asset wealth concentration

capital misallocation toward land

reduced sovereign capacity for capital formation

infrastructure underinvestment

increased external financial exposure

potential productivity stagnation.

LAYER 14 — PANEL THREE REPRESENTATION

Panel Three visualises the balance-sheet consequences of the system.

Green line:

sovereign and public credit.

Brown line:

private bank credit.

Red line:

external liabilities.

The rising brown line reflects the displacement of sovereign development credit by mortgage-dominated private credit creation.

Panel Three therefore illustrates the displacement of the capital constitution of the economy.

LAYER 15 — CONSTITUTIONAL DIAGNOSIS

If institutional design simultaneously:

• removes sovereign mechanisms for directing capital formation

• transfers credit creation authority to private banks

• governs monetary policy using measurement systems that exclude housing-credit dynamics

• discourages public capital investment through fiscal accounting rules

• allows mortgage-dominated credit allocation

• links domestic leverage to external liabilities

then the state’s ability to steward national capital formation becomes structurally impaired.

FINAL CONSTITUTIONAL QUESTION

Is an economic architecture that transfers the practical power of credit creation and allocation away from sovereign institutions, while obscuring its consequences through measurement systems, consistent with the fiduciary responsibilities of democratic governance?

TBLR CORE LEDGER

MEASUREMENT CONSTITUTION MODULE

I. GOVERNING PRINCIPLE

Economic measurement systems are not neutral descriptive tools.

They perform three constitutional functions.

They define what counts as an economic problem.

They determine when policy institutions respond.

They influence how burdens and benefits are distributed across society.

Therefore:

measurement systems form part of the constitutional architecture of economic governance.

II. DEFINITION — MEASUREMENT CONSTITUTION

The measurement constitution is the set of official indicators, accounting rules, and statistical classifications that determine how economic reality is recognised by policy institutions.

It includes:

• inflation measures

• fiscal measures

• debt measures

• balance-sheet classifications

• cost-of-living measures

• sectoral lending classifications.

These measures shape the operation of:

• central banking

• fiscal policy

• regulatory policy

• public investment decisions.

III. CONSTITUTIONAL STATUS OF MEASUREMENT

A measurement regime has constitutional significance when it performs any of the following functions:

triggers policy responses

constrains or enables public action

defines official economic success or failure

allocates burdens across sectors or social groups.

By this standard, measurement systems such as CPI, HLPI, debt ratios, and public-balance-sheet rules are not merely statistical.

They are governing instruments.

IV. HONEST WEIGHTS AND MEASURES

The principle of honest weights and measures is one of the oldest doctrines in economic governance.

It appears across:

• ancient Near Eastern trade systems

• biblical law

• classical legal traditions

• Roman market regulation

• medieval and early modern European law.

Its core principle is simple:

if the measure is false, the governance built upon it is distorted.

In modern economic systems, the analogue of weights and measures is:

• inflation indices

• debt metrics

• accounting standards

• official price classifications.

Therefore:

If official measurement systems omit the dominant drivers of economic pressure, governance fails the honest-weights principle.

V. CPI AS A CONSTITUTIONAL MEASURE

In New Zealand the Consumer Price Index is the principal measure used for inflation targeting.

Because it is used to guide monetary policy, CPI performs a constitutional role.

It influences:

• official perceptions of inflation

• Reserve Bank responses

• wage and benefit expectations

• political narratives about economic stability.

Therefore CPI is not merely descriptive.

It is an operative constitutional metric.

VI. CPI SCOPE AND LIMITS

CPI is designed as a consumer price index.

It measures price changes in a basket of household consumption items.

It does not directly measure:

• land prices

• house purchase prices

• mortgage principal repayments

• mortgage interest payments.

Housing enters CPI mainly through:

• rents

• maintenance

• insurance

• local government rates.

Therefore CPI does not directly capture the full cost structure of a mortgage-credit-driven housing economy.

VII. CPI AVERAGING STRUCTURE

CPI aggregates very different categories of prices into a single average.

These include:

Tradable goods

• electronics

• clothing

• appliances

• imported manufactures

Essential domestic costs

• food

• rent and housing-related costs

• insurance

• utilities

• domestic services

• transport-related essentials

Administrative and regulated costs

• local government rates

• network utility charges

• compliance-driven service costs

• infrastructure-related charges

• licensing and regulated fees embedded in household expenses

Because CPI is an average, falling tradable goods prices can offset rising essential and administrative domestic costs.

Therefore CPI can remain relatively stable while lived household cost pressure rises.

VIII. DUAL MASKING MECHANISM

The New Zealand measurement system contains two distinct masking effects.

A. Averaging Mask

Rising essential domestic costs are averaged against cheaper tradable goods.

This can suppress headline CPI even while household essentials become more expensive.

B. Exclusion Mask

Key housing-credit costs are not directly included in headline CPI.

These include:

• land prices

• mortgage principal

• mortgage interest.

This means the dominant pressures in a credit-driven housing system can remain structurally underrepresented in the policy index.

IX. CONSEQUENCE — POLICY INFLATION VS LIVED INFLATION

Because of the averaging mask and exclusion mask, there can be a divergence between:

Policy inflation

Inflation as measured by CPI and used by monetary authorities.

Lived inflation

The actual increase in household financial pressure experienced through:

• food

• rent or housing-related costs

• insurance

• utilities

• administrative charges

• debt-servicing pressure in household budgets.

This divergence weakens policy feedback.

The state can record inflation as “under control” while households experience rising economic stress.

X. HLPI AS A CORRECTIVE MEASURE

The Household Living-Cost Price Index provides a different perspective.

HLPI tracks the cost pressures faced by households more directly, including mortgage-interest effects for relevant household groups.

Therefore HLPI is closer than CPI to lived inflation for leveraged households.

This does not make HLPI “better” in every context.

It means that CPI and HLPI serve different constitutional functions.

CPI is a macro policy index.

HLPI is a household-cost index.

Failure to distinguish them creates analytical confusion.

XI. MEASUREMENT AND MONETARY POLICY

The Reserve Bank adjusts the Official Cash Rate in response to inflation signals.

If the inflation signal is structurally incomplete, then monetary policy operates with incomplete information.

Therefore:

If CPI excludes key housing-credit dynamics while the banking system is dominated by mortgage lending, monetary policy can systematically underreact to the dominant inflationary mechanism in the economy.

This is a structural policy problem, not a one-off error.

XII. MEASUREMENT AND DISTRIBUTION

Measurement regimes are also distributive.

If policy is guided by an index that underweights or excludes the dominant pressures on some households, then policy will tend to privilege the conditions of households less exposed to those pressures.

In a mortgage-credit-driven economy this means:

households exposed to food, housing, insurance, utilities, rates, and debt-service stress may experience higher lived inflation than headline CPI suggests.

Therefore measurement systems affect distributional justice.

XIII. MEASUREMENT AND FISCAL GOVERNANCE

The measurement constitution is not limited to CPI.

It also includes fiscal accounting metrics such as:

• debt-to-GDP ratios

• liability measures

• accrual accounting categories.

When public capital investment appears primarily through liability measures, fiscal debate can treat investment as debt rather than as capital formation.

This links measurement directly to public-investment capacity.

Thus:

the measurement constitution governs both monetary and fiscal action.

XIV. MEASUREMENT FAILURE TEST

A measurement regime fails constitutionally when all of the following are present:

the metric is used to trigger policy

the metric excludes dominant economic pressures

policy institutions rely heavily on that metric

the excluded pressures materially affect households or capital formation.

Under those conditions, measurement failure becomes a constitutional problem rather than a technical issue.

XV. THE NEW ZEALAND CASE

In the New Zealand Treasury Trap architecture:

• CPI is the principal inflation metric

• OCR policy targets CPI

• private banks dominate credit creation

• mortgage lending dominates bank lending

• housing-credit costs are not fully represented in CPI

• essential and administrative domestic costs can be diluted by cheaper tradables.

Therefore the measurement regime can register stability while the underlying economic structure becomes more leveraged, more property-dominated, and more burdensome for households.

XVI. FORMAL PROPOSITION

If

monetary policy is governed primarily by CPI

CPI excludes land and mortgage-credit dynamics

CPI averages rising domestic essentials against cheaper tradables

banks allocate most credit toward housing collateral

then

headline inflation stability does not imply structural economic stability.

XVII. CONSTITUTIONAL CONCLUSION

Measurement is not a neutral mirror of the economy.

Measurement governs the perception of the economy, and perception governs institutional response.

Therefore:

the measurement constitution is part of the economic constitution.

If the measurement constitution fails to register the dominant forces shaping household burden and capital formation, then the state’s fiduciary duty, duty of care, and obligation to maintain honest weights and measures are all placed in question.

XVIII. LEDGER USE RULE

Whenever a future argument refers to inflation, cost of living, or monetary stability, it must distinguish:

• CPI

• HLPI

• tradable prices

• essential domestic costs

• administrative and regulated costs

• excluded housing-credit costs.

Failure to distinguish these constitutes a measurement smudge.

TBLR DEFINITIONS LOCK v3

Canonical Economic Terms for Constitutional Analysis

1 — Sovereign Credit Creation

Definition

Sovereign credit creation is the expansion of purchasing power through balance-sheet operations conducted by public monetary or financial institutions under public authority.

Mechanisms may include:

• central bank credit extended to the state

• lending by publicly owned financial institutions

• credit issued through development finance agencies.

Functional property

Sovereign credit creation increases financial assets within the domestic economy without requiring prior private savings.

Allocation decisions are governed by public institutions rather than private lenders.

2 — Sovereign Borrowing

Definition

Sovereign borrowing occurs when a government issues financial securities and receives funds from investors.

Typical instruments include government bonds.

Mechanism

Borrowing transfers existing financial resources from lenders to the state.

Borrowing does not itself create new money unless associated with banking or central bank operations.

3 — Public Development Credit

Definition

Public development credit refers to credit issued or directed through publicly owned financial institutions for the purpose of supporting national development.

Examples historically include:

• state housing finance programmes

• public agricultural lending systems

• national development banks.

Economic function

Public development credit directs financing toward capital formation in areas such as:

• infrastructure

• housing construction

• industrial development

• strategic national capabilities.

4 — Private Bank Credit Creation

Definition

Commercial banks create deposits when issuing loans.

The lending process simultaneously creates:

• a loan asset on the bank balance sheet

• a deposit liability representing newly created money.

System role

In modern financial systems private banks are the dominant creators of new credit.

The sectors receiving bank credit therefore shape the pattern of investment within the economy.

5 — Bank Funding

Definition

Bank funding refers to the liabilities used to finance bank balance sheets.

These include:

• customer deposits

• wholesale borrowing

• offshore funding

• bank capital instruments.

Distinction

Credit creation occurs when loans are issued.

Funding refers to the sources supporting the bank’s balance sheet.

These are analytically separate processes.

6 — Credit Allocation

Definition

Credit allocation refers to the distribution of newly created credit across sectors of the economy.

Allocation may occur through:

• private lending decisions

• regulatory guidance

• publicly directed development credit programmes.

Economic importance

Credit allocation determines which sectors receive financing and therefore shapes the structure of economic activity.

7 — Credit Direction

Definition

Credit direction refers to institutional mechanisms that guide credit allocation toward specific sectors.

Examples include:

• development banks

• state-directed lending programmes

• sectoral lending quotas

• government-supported industrial finance schemes.

8 — Capital Formation

Definition

Capital formation is the creation of new productive assets that increase the economy’s capacity to produce goods and services.

Examples include:

• infrastructure construction

• industrial machinery

• energy generation systems

• transport networks

• technological research capability.

9 — Asset Transfer vs Capital Formation

Definition

Transactions involving existing assets may transfer ownership without creating new productive capacity.

Examples include:

• purchase of existing land

• purchase of existing housing stock.

Such transactions primarily redistribute asset ownership rather than create new capital.

10 — Capital Misallocation

Definition

Capital misallocation occurs when credit flows disproportionately toward activities that do not increase productive capacity.

Examples include:

• speculative land purchases

• financial asset speculation

• leverage applied primarily to asset price inflation.

Persistent capital misallocation can reduce long-term economic growth.

11 — Land Price Capitalisation

Definition

Land price capitalisation is the process by which expected future income from land ownership becomes incorporated into current land prices.

Mechanism

Expanded credit availability increases purchasing power in land markets.

Higher purchasing power raises land prices.

Rising land prices increase collateral values and borrowing capacity.

This produces a reinforcing cycle:

credit expansion → higher land prices → increased borrowing → further credit expansion.

12 — Mortgage Credit Expansion

Definition

Mortgage credit expansion refers to the growth of bank lending secured against residential or commercial property.

Mortgage lending increases purchasing power in land markets and contributes to asset price inflation.

13 — Mortgage–Funding Transmission

Definition

Mortgage-funding transmission refers to the mechanism through which domestic mortgage lending leads to offshore borrowing by banks.

Sequence

mortgage lending expands

→ bank balance sheets grow

→ banks seek additional funding

→ offshore wholesale borrowing increases

→ external liabilities rise.

14 — Household Leverage

Definition

Household leverage refers to the ratio of household debt to household income or assets.

Mortgage borrowing typically constitutes the largest component of household leverage.

15 — External Liabilities

Definition

External liabilities represent financial obligations owed by domestic residents to foreign investors or lenders.

Sources include:

• offshore borrowing

• foreign ownership of domestic assets.

External liabilities generate future income outflows.

16 — Net Primary Income Balance

Definition

Net primary income measures income flows between residents and non-residents arising from investment and employment.

A deficit occurs when payments to foreign investors exceed income received from overseas assets.

Typical components include:

• interest payments

• dividend payments

• profit repatriation.

17 — Inflation Measurement

Definition

Inflation measurement refers to statistical indicators used to track price changes across the economy.

In New Zealand the primary indicator is the Consumer Price Index produced by

Statistics New Zealand.

Measurement scope

CPI measures consumer goods and services.

It does not directly measure:

• land prices

• asset prices

• mortgage principal payments

• mortgage interest costs.

18 — Monetary Policy

Definition

Monetary policy refers to central bank actions intended to influence credit conditions within the economy.

In New Zealand the central bank is the

Reserve Bank of New Zealand.

The primary instrument is the Official Cash Rate.

Policy scope

Interest-rate policy primarily affects the price of credit.

Credit allocation decisions remain largely determined by lending institutions.

19 — The Treasury Trap

Definition

The Treasury Trap describes a structural condition in which:

• sovereign mechanisms for directing development credit are removed

• private banks dominate credit creation

• credit allocation gravitates toward property collateral

• inflation measurement excludes housing-credit dynamics

• fiscal accounting discourages sovereign investment.

Under these conditions credit expansion primarily inflates asset prices rather than productive capital formation.

20 — Panel Three

Definition

Panel Three is a balance-sheet representation of the credit architecture of the economy.

It distinguishes three financial trajectories:

Green line — sovereign and public credit

Brown line — residual public credit under post-reform fiscal constraints

Red line — external or foreign liabilities.

Interpretation

Panel Three illustrates the collapse of sovereign development credit and the simultaneous rise of external financial obligations.

The chart visualises the shift in the locus of leverage from public balance sheets toward private and external balance sheets.

Closing Statement

The definitions in this module establish precise distinctions between:

• sovereign credit creation

• sovereign borrowing

• private bank credit creation

• credit allocation

• capital formation

• asset price inflation.

These distinctions prevent analytical confusion and protect the integrity of the constitutional analysis.

21 — Official Cash Rate (OCR)

Definition

The Official Cash Rate is the policy interest rate set by the

Reserve Bank of New Zealand.

It represents the rate at which banks can borrow or deposit settlement cash with the central bank overnight.

Function

The OCR influences short-term interest rates throughout the financial system.

Changes in the OCR affect:

• mortgage interest rates

• business lending rates

• deposit rates.

Policy scope

The OCR primarily influences the price of credit.

It does not directly determine:

• the quantity of credit created by banks

• the allocation of credit across sectors of the economy.

22 — Consumer Price Index (CPI)

Definition

The Consumer Price Index is the primary inflation indicator produced by

Statistics New Zealand.

It measures the average price change of a basket of consumer goods and services purchased by households.

CPI measures consumer price averages, not the structural cost dynamics of housing, credit, and domestic services.

Coverage

CPI measures prices of items such as:

• food

• transport

• energy

• rent

• household goods

• services.

Exclusions

CPI does not directly measure:

• land prices

• house purchase prices

• mortgage principal repayments

• mortgage interest payments.

Implication

Because housing credit dynamics are not fully represented in CPI, large increases in mortgage borrowing and house prices may occur without equivalent increases in measured CPI inflation.

Structural Limitation of CPI-Based Inflation Targeting

Inflation targeting based primarily on CPI has several structural limitations.

CPI does not fully capture several important economic dynamics.

These include:

• asset price inflation, including land and housing prices

• credit allocation patterns within the financial system

• land price capitalisation driven by mortgage credit expansion

• household financing costs such as mortgage principal payments

• divergences between domestic cost pressures and imported goods prices.

Tradables Averaging Mechanism

CPI aggregates price movements across both domestically produced goods and imported tradable goods.

When prices of imported manufactured goods fall — for example electronics, appliances, or clothing — these declines can offset rising prices of domestic essentials.

Examples of domestic costs that may rise include:

• housing

• construction

• insurance

• local services

• utilities.

As a result, CPI may remain relatively stable even while the cost of essential domestic goods and services increases.

Policy Implication

Because CPI averages these components together, inflation targeting based solely on CPI may provide incomplete feedback regarding structural price pressures within the domestic economy.

Why This Matters

This mechanism explains how the following can occur simultaneously:

stable CPI

+

rising housing costs

+

rising mortgage debt

+

rising household cost pressures

The result is a divergence between:

policy inflation

vs

lived inflation

which weakens policy feedback.

23 — Household Living-Cost Price Index (HLPI)

Definition

The Household Living-Cost Price Index is a statistical measure produced by

Statistics New Zealand.

HLPI estimates the change in the cost of living experienced by households by tracking changes in prices of items households actually pay.

Coverage

HLPI includes components such as: